306

Investing

Investing is putting money to work for you. Some investments involve little risk, for little reward. Other investments involve great risk, for great reward—or loss. Because of the rate of inflation, money that is not invested in some way actually loses value over time.

Planning Investments

You can use the inquiry process to set up investments. Here are the steps to follow when investing:

Questioning: What do you want your money to do? Do you want it to be secure? Do you want it to earn as much as it can? Do you want quick returns, or are you investing for the long term? What options are available to you? | Question |

Planning: Think of the types of investment instruments you could use—savings, CDs, bonds, stocks, mutual funds, retirement accounts. Consider the strengths and weaknesses of each type. | Plan |

Researching: Discover which financial adviser has the best track record. Learn which stocks are performing best. Study markets. Investigate tax strategies. | Research |

Creating: Invest in an appropriate mix of different assets. With the help of a financial adviser, assemble a portfolio that matches your risk profile. Keep your records in a safe and easy-to-access location. | Create |

Improving: Monitor your investments. Note the instruments that deliver the dividends you want or the security you need. Adjust your investments to best match your goals. | Improve |

Presenting: Use the dividends from your investments as ready capital, or reinvest them to grow your wealth. | Present |

Your Turn Begin your investment planning by writing answers to the questions listed above under “Questioning.”

307

Understanding Investment Instruments

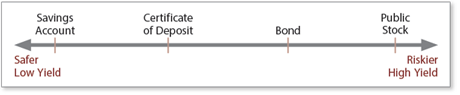

Investing starts with a simple savings account, which protects money and provides modest interest income. Other investment strategies offer less protection but can provide bigger returns. In that sense, investment strategies can be ranked in a continuum from secure, low-yield options to risky, high-yield options.

- Savings accounts at most banks and credit unions are federally insured for up to $250,000. The institution lends your money out to others and gives you a portion of the interest they make from the loans.

- Retirement accounts such as 401(k)s, IRAs, pensions, and profit-sharing accounts allow investors to set aside money with some tax advantages. The money is often professionally invested in a portfolio that represents the investor’s individual strategy—from low-risk/low-yield instruments to high-risk/high-yield instruments, or a combination of the whole range.

- Certificates of deposit (CDs) are issued by banks and credit unions and indicate that the bearer has invested money for a specified period between three months and six years, to be repaid at an interest rate established at the time the CD is issued. Early withdrawal of the money can be subject to penalties. This federally insured instrument is low risk and low yield.

- Bonds are loans made by the bondholder for a specified period of time, during which the bondholder receives interest at intervals (monthly, semiannually, or annually). One way bonds differ from stocks is that a bondholder lends money while a stockholder buys shares of a business.

- Stocks are securities that establish ownership in a company and represent claims on part of the company’s assets and earnings.

- Holders of common stock usually can vote at shareholder meetings.

- Holders of preferred stock generally cannot vote at shareholder meetings but receive a higher claim on assets and usually receive dividends before common stockholders.

- Mutual funds are professionally managed pools of money from a large group of investors. The money is invested in a variety of securities in an attempt to produce capital gains and income for the investors. Mutual funds are federally regulated.

Your Turn Which type of investment above would be most helpful to you right now? Why? Which type of investment will be most helpful to you in 10 years? In 50 years? Why?